Tags & Description

Accounting

The process of identifying, measuring, recording, and communicating financial information about a company’s activities so decision-makers can make informed decisions.

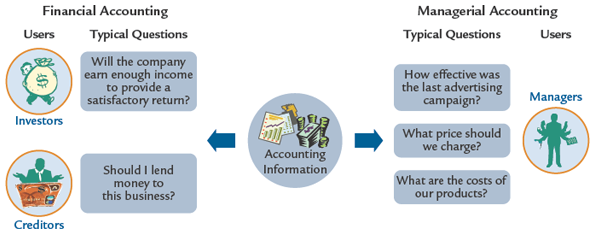

Financial Accounting

Accounting and reporting to satisfy the outside demand (primarily investors and creditors) for accounting information.

Sole Proprietorship

A business owned by one person.

Partnership

A business owned jointly by two or more individuals.

Corporation

A company chartered by the state to conduct business as an “artificial person” and owned by one or more stockholders.

Creditor

The person to whom money is owed.

Stockholders’ Equity

The owners’ claims against the assets of a corporation after all liabilities have been deducted.

Revenue

The increase in assets that results from the sale of products or services.

Expenses

The cost of assets used, or the liabilities created, in the operation of the business.

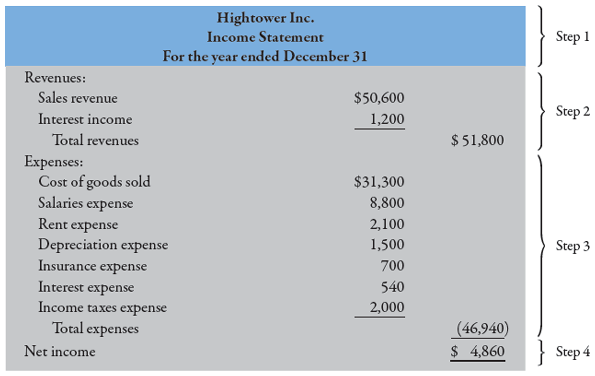

Net Income

The excess of a company’s revenue over its expenses during a period of time.

Net Loss

The excess of a company’s expenses over its revenues during a period of time.

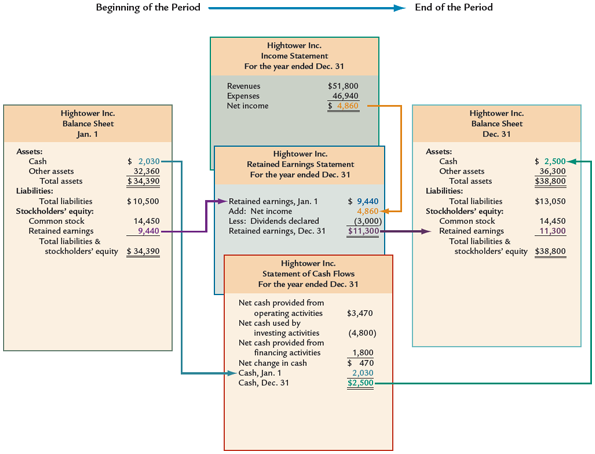

Financial Statements

A set of standardized reports in which the detailed transactions of a company’s activities are reported and summarized so they can be communicated to decision-makers.

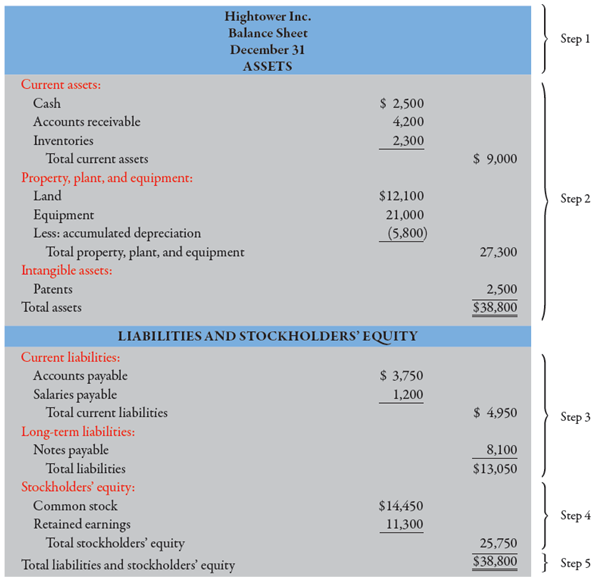

Balance Sheet

A financial statement that reports the resources (assets) owned by a company and the claims against those resources (liabilities and stockholders’ equity) at a specific point in time.

Income Statement

A financial statement that reports the profitability of a business over a specific period of time.

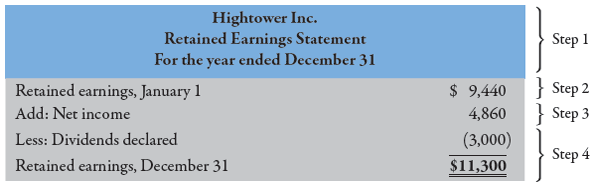

Retained Earnings Statement

A financial statement that reports how much of the company’s income was retained in the business and how much was distributed to owners for a period of time.

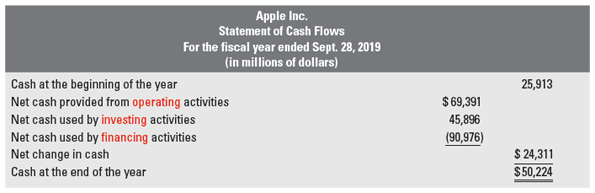

Statement of Cash Flows

A financial statement that provides relevant information about a company’s cash receipts (inflows of cash) and cash payments (outflows of cash) during an accounting period.

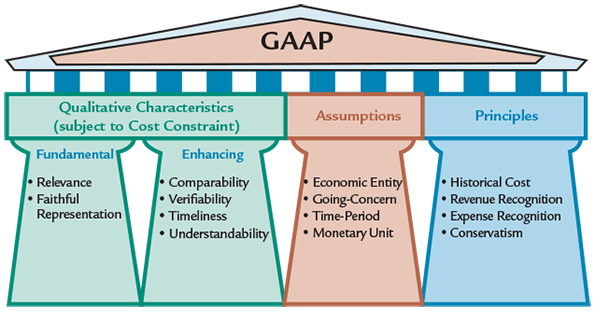

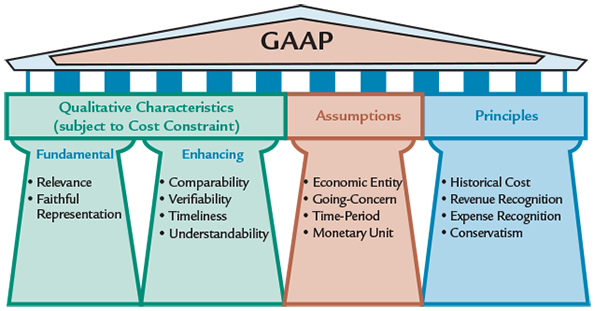

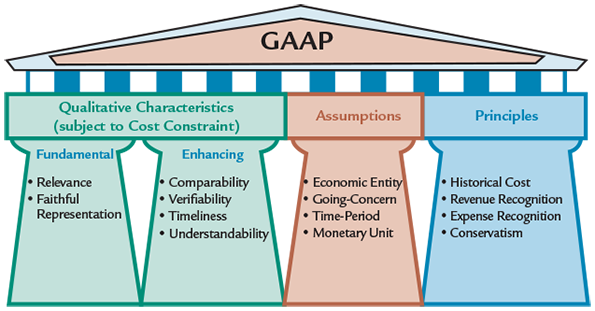

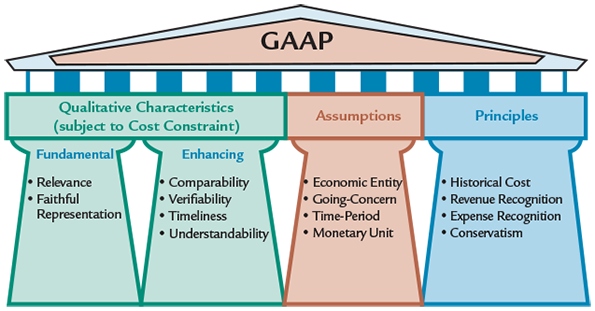

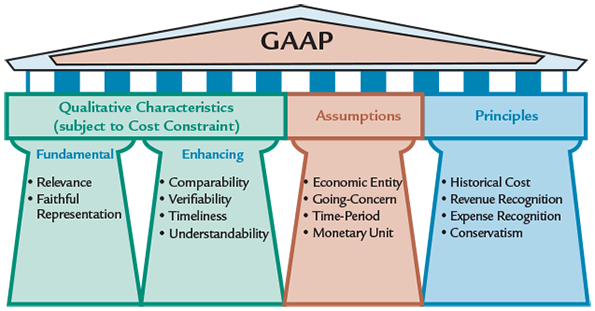

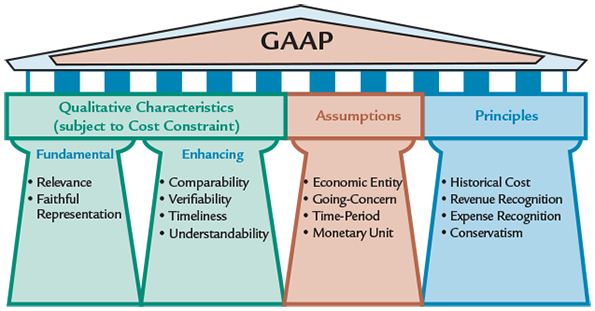

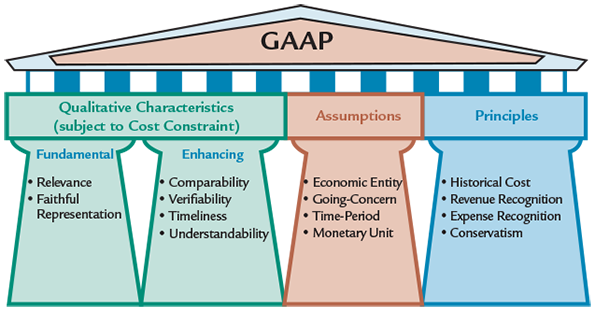

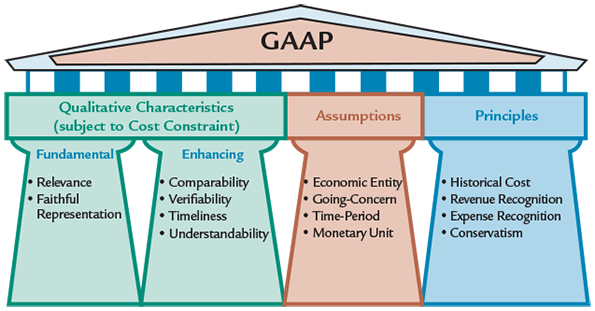

Generally Accepted Accounting Principles (GAAP)

The rules and conventions used to prepare financial statements. By following these rules and conventions financial statements users can compare performance over time and across companies.

Securities and Exchange Commission (SEC)

The federal agency established by Congress to regulate securities markets and ensure effective public disclosure of accounting information. The SEC has the power to set accounting rules for publicly traded companies.

Financial Accounting Standards Board (FASB)

The primary accounting standard-setter in the United States which has been granted this power to set standards by the Securities and Exchange Commission.

International Accounting Standards Board (IASB)

An independent, privately funded accounting standard-setting body with the goal of developing a single set of high-quality accounting standards that result in transparent and comparable information reported in general purpose financial statements.

International Financial Reporting Standards (IFRS)

A general term that describes an international set of generally accepted accounting standards.

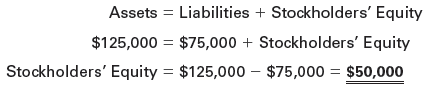

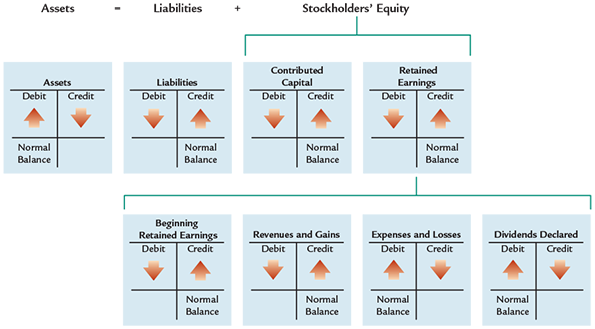

Fundamental Accounting Equation

Assets = Liabilities + Stockholders’ Equity

The left side of the accounting equation shows the assets, or economic resources, of a company. The right side of the accounting equation indicates who has a claim on the company’s assets.

Fiscal Year

An accounting period that runs for one year.

Current Assets

Cash and other assets that are reasonably expected to be converted into cash within one year or one operating cycle, whichever is longer.

Operating Cycle

The average time that it takes a company to purchase goods, resell them, and collect the cash from customers.

Long-term Investments

Investments that the company expects to hold for longer than one year. This includes land or buildings that a company is not currently using in operations, as well as debt and equity securities.

Property, plant, and equipment

The tangible, long-lived, productive assets used by a company in its operations to produce revenue. This includes land, buildings, machinery, manufacturing equipment, office equipment, and furniture.

Intangible Assets

Similar to property, plant, and equipment in that they provide a benefit to a company over a number of years; however, these assets lack physical substance.

Current Liabilities

Obligations that require a firm to pay cash or another current asset, create a new current liability, or provide goods or services within one year or one operating cycle, whichever is longer.

Long-term Liabilities

The obligations of the company that will require payment beyond one year or the operating cycle, whichever is longer.

Contributed Capital

The owners’ contributions of cash and other assets to the company (includes the common stock of a company).

Retained Earnings

Ending Retained Earnings = Beginning Retained Earnings + Net Income - Dividends Declared

The accumulated earnings (or losses) over the entire life of the corporation that have not been paid out in dividends.

Capital

A company’s assets less its liabilities. Also known as stockholders’ equity.

Liquidity

A company’s ability to pay obligations as they become due.

Working Capital

A measure of liquidity computed as: Current Assets – Current Liabilities.

Current Ratio

A measure of liquidity that is computed as: Current Assets ÷ Current Liabilities.

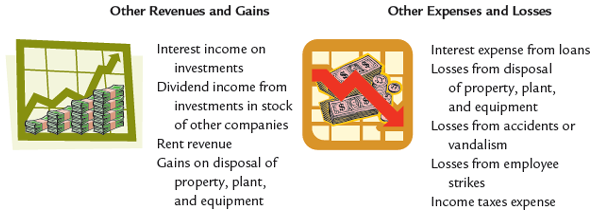

Gains

Increases in net assets that occur from peripheral or incidental transactions.

Losses

Decreases in net assets that occur from peripheral or incidental transactions.

Gross Margin (or gross profit)

Gross Margin = Net Sales - Cost of Goods Sold

A key performance measure that is computed as sales revenue less cost of goods sold.

Income from Operations

Income from Operations = Gross Margin - Operating Expenses

Gross margin less operating expenses. This represents the results of the core operations of the business.

Operating Expenses

The expenses the business incurs in selling goods or providing services and managing the company.

Nonoperating Activities

Revenues and expenses from activities other than the company’s principal operations.

Net Profit Margin

Net Profit Margin = Net Income ÷ Sales (or Service) Revenue

A useful measure of a company’s ability to generate profit.

Cash Flows from Operating Activities

Any cash flows directly related to earning income, including cash sales and collections of accounts receivable as well as cash payments for goods, services, salaries, and interest.

Cash Flows from Investing Activities

The cash inflows and outflows that relate to acquiring and disposing of operating assets, acquiring and selling investments (current and long-term), and lending money and collecting loans.

Cash Flows from Financing Activities

Any cash flow related to obtaining resources from creditors or owners, which includes the issuance and repayment of debt, common and preferred stock transactions, and the payment of dividends.

Articulation

Describes the linkages between the financial statements. Specifically, the income statement links the beginning and ending balance sheet through retained earnings; the statement of shareholders’ equity links the beginning and ending balances of equity; and the statement of cash flows links the beginning and ending balances of cash.

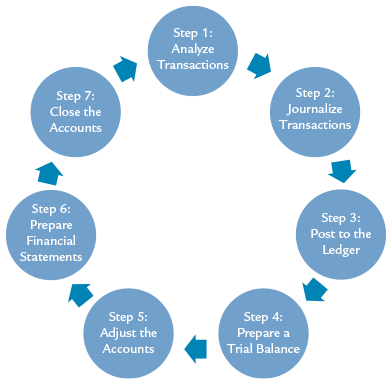

Accounting Cycle

The procedures that a company uses to transform the results of its business activities into financial statements.

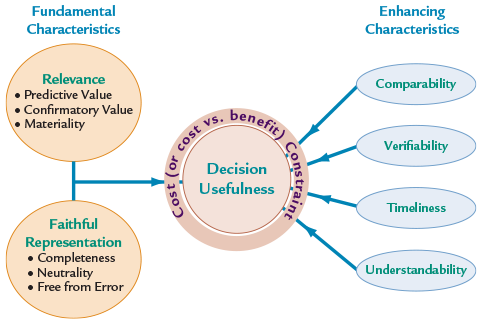

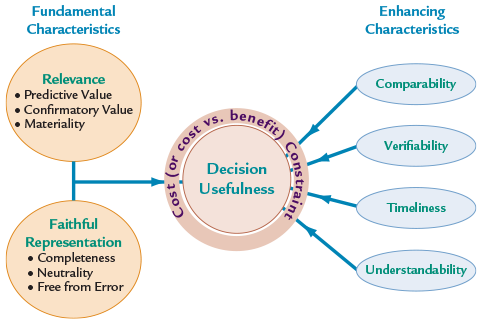

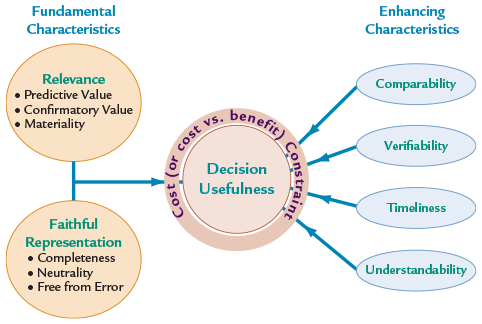

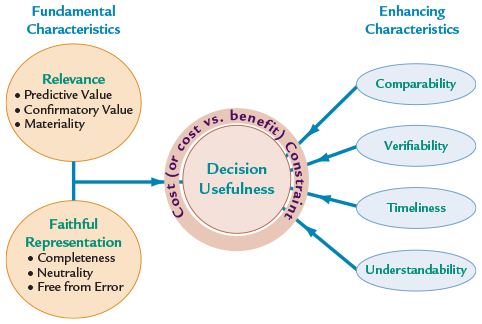

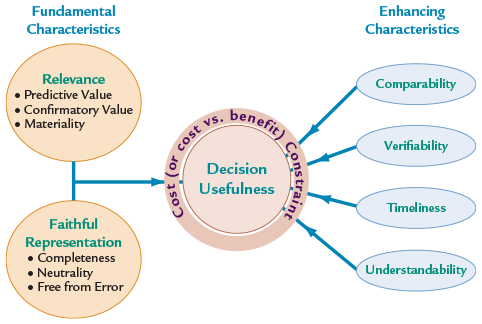

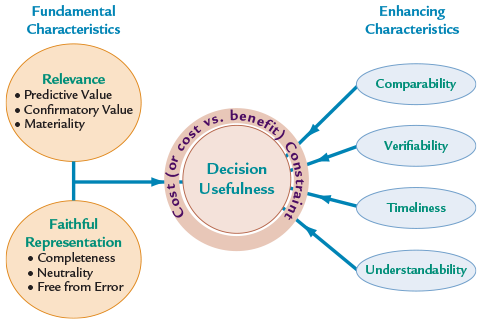

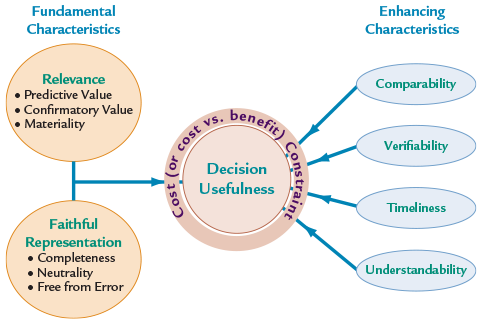

Comparability

One of the four qualitative characteristics that useful information should possess. Information has ______ if it allows comparisons to be made between companies.

Conservatism Principle

A principle which states that when more than one equally acceptable accounting method exists, the method that results in the lower assets and revenues or higher liabilities and expenses should be selected.

Consistency

One of the four qualitative characteristics that useful information should possess. Refers to the application of the same accounting principles by a single company over time.

Cost Constraint

Qualitative characteristic of useful information that states that the benefit received from accounting information should be greater than the cost of providing that information.

Economic Entity Assumption

One of the four basic assumptions that underlie accounting that assumes each company is accounted for separately from its owners.

Expense Recognition Principle

This principle requires that an expense be recorded and reported in the same period as the revenue it helped generate.

Faithful Representation

Qualitative characteristic of information stipulating it should be complete, neutral, and free from error.

Full Disclosure

A policy that requires any information that would make a difference to financial statement users to be revealed.

Historical Cost Principle

A principle that requires the activities of a company to be initially measured at their cost—the exchange price at the time the activity occurs.

Relevance

One of the four qualitative characteristics that useful information should possess. Accounting information is said to be relevant if it is capable of making a difference in a business decision by helping users predict future events or by providing feedback about prior expectations. Relevant information must also be provided in a timely manner.

Revenue Recognition Principle

A principle that requires revenue to be recognized or recorded in the period in which it is earned and the collection of cash is reasonably assured.

Timeliness

Quality of information where it is available to users before it loses its ability to influence decisions.

Time-period Assumption

One of the four basic assumptions that underlie accounting that allows the life of a company to be divided into artificial time periods so net income can be measured for a specific period of time (e.g., monthly, quarterly, annually).

Understandability

Quality of information whereby users with a reasonable knowledge of accounting and business can comprehend the meaning of that information.

Verifiability

Quality of information indicating the information is verifiable when independent parties can reach a consensus on the measurement of the activity.

Events

Make up the multitude of activities in which companies engage. External events result from an exchange between the company and another outside entity, and internal events result from a company’s own actions that do not involve other companies.

Transaction

Any event, external or internal, that is recognized in the financial statements.

Transaction Analysis

The process of determining the economic effects of a transaction on the elements of the accounting equation.

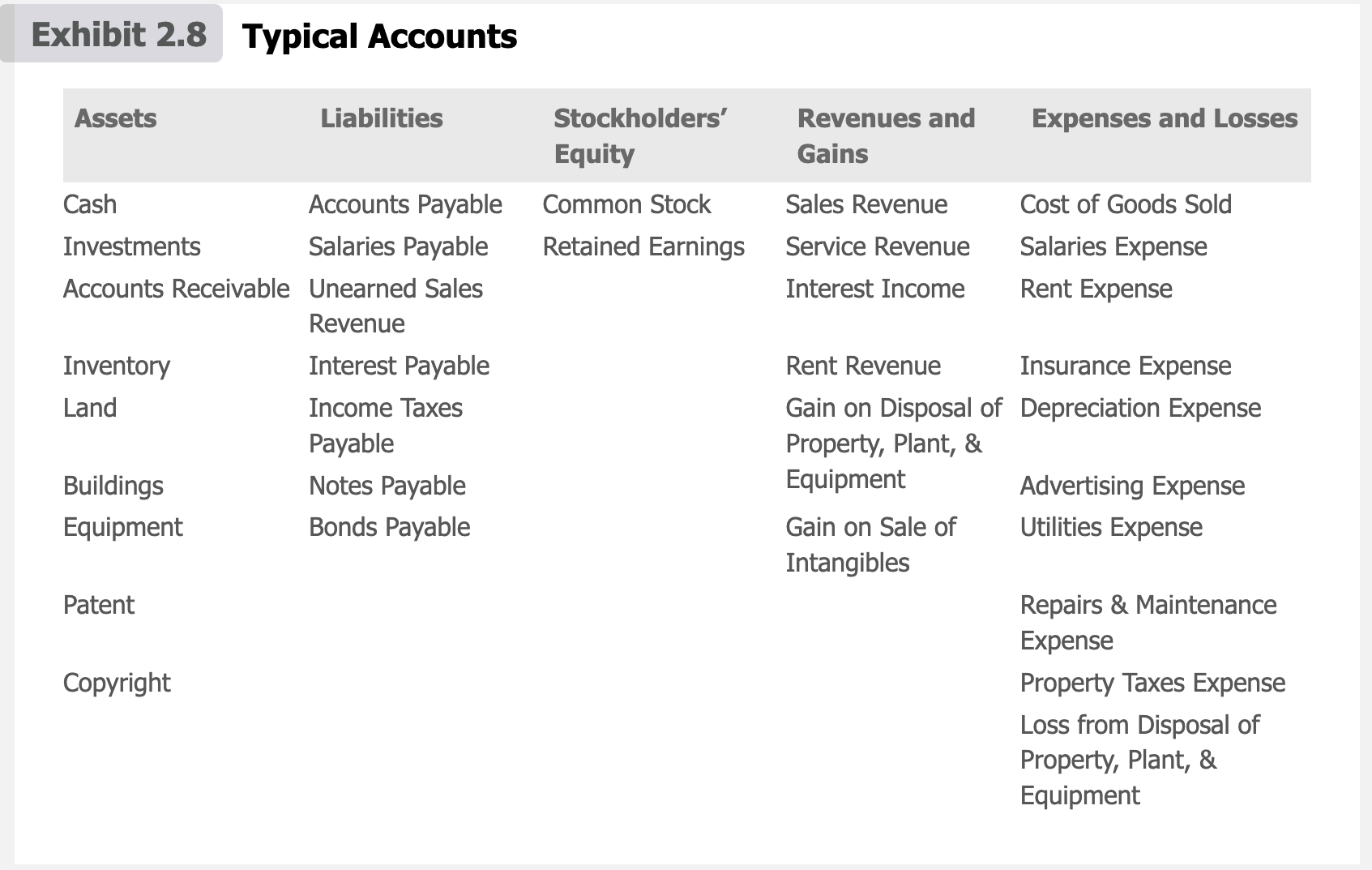

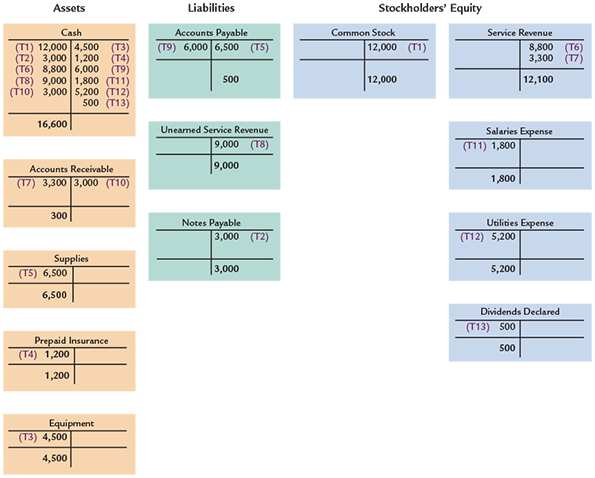

Account

A record of increases and decreases in each of the basic elements of the financial statements (each of the company’s asset, liability, stockholders’ equity, revenue, expense, gain, and loss items).

Chart of Accounts

The list of accounts used by a company.

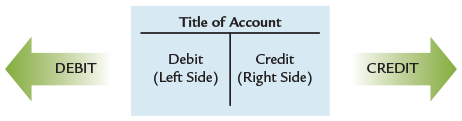

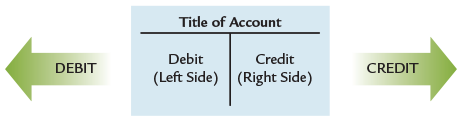

Credit

The right side of a T-account; alternatively, credit may refer to the act of entering an amount on the right side of an account (decreases cash).

Debit

The left side of a T-account; alternatively, debit may refer to the act of entering an amount on the left side of an account (increases cash).

Normal Balance

The type of balance expected of an account based on its effect on the fundamental accounting equation. Assets, expenses, and dividends have normal debit balances while liabilities, stockholders’ equity, and revenues have normal credit balances.

T-account

A graphical representation of an account that gets its name because it resembles the capital letter T. A T-account is a two-column record that consists of an account title and two sides divided by a vertical line—the left side is called the debit side and the right side is called the credit side.

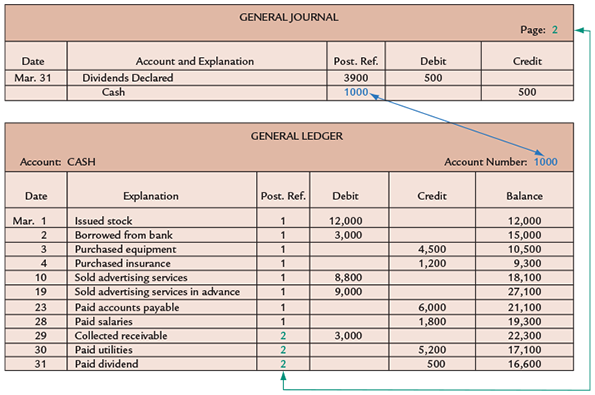

Journal

A chronological record showing the debit and credit effects of transactions on a company.

Journal Entry

A record of a transaction that is made in a journal so that the entire effect of the transaction is contained in one place.

General Ledger

A collection of all the individual financial statement accounts that a company uses in its financial statements.

Posting

The process of transferring information from journalized transactions to the general ledger.

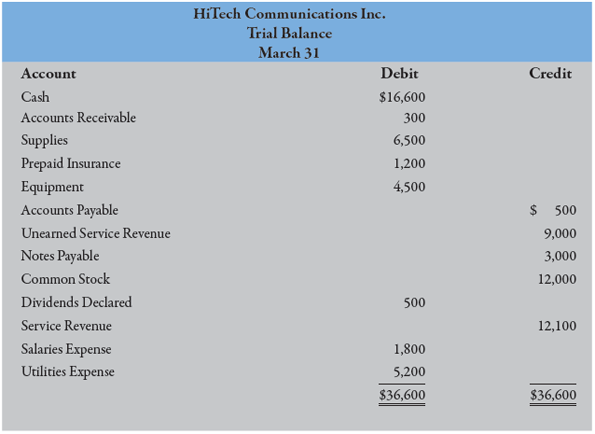

Trial Balance

A list of all active accounts and each account’s debit or credit balance.