Ch 16 - Macroeconomic Equilibrium

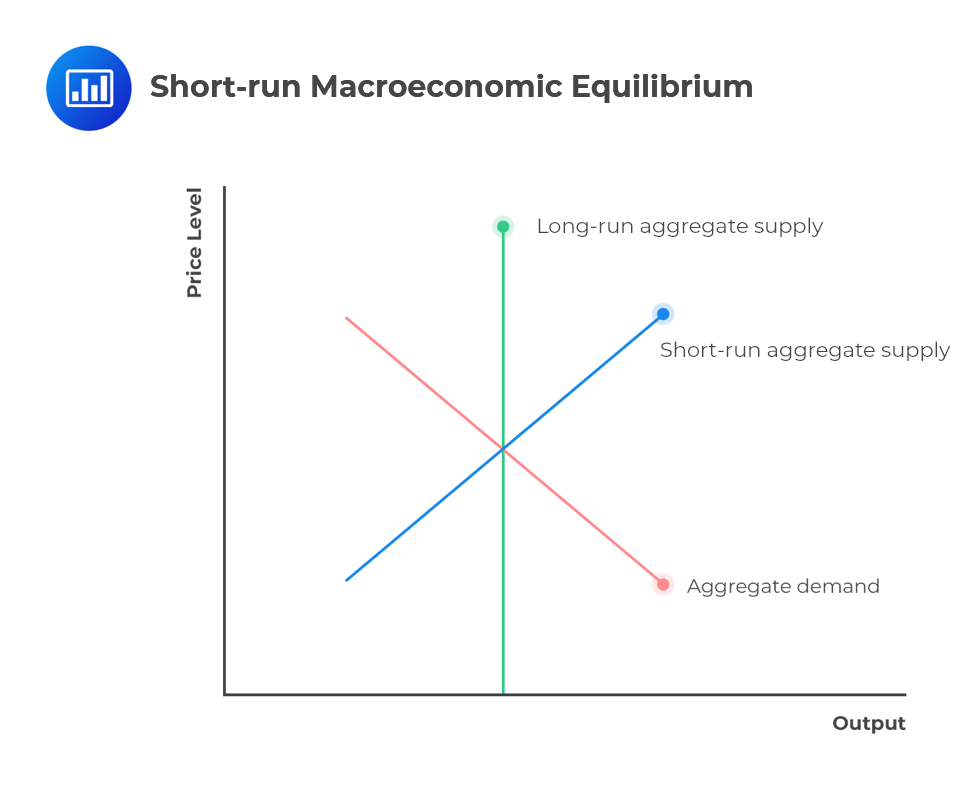

Equilibrium: the point which demand is equal to supply

Determines the average price and quantity produced and sold on the market

The economy is in short run equilibrium when aggregate demand equals aggregate supply

The output produced by the economy is exactly equal to the total demand in the economy, so there is no reason for producers to change their levels of output

When aggregate demand is equal to aggregate supply, there us no upwards/downwards pressure on the price level

No inflationary/deflationary pressure

There is equilibrium as long as nothing influences AD or AS

New-classical perspective: Relationship between macroeconomic equilibrium and productive capacity**:**

In short run: equilibrium could operate in the short run equilibrium at below their potential output

In long run: the economy could return to its maximum potential output (equilibrium would be at AD + LRAS)

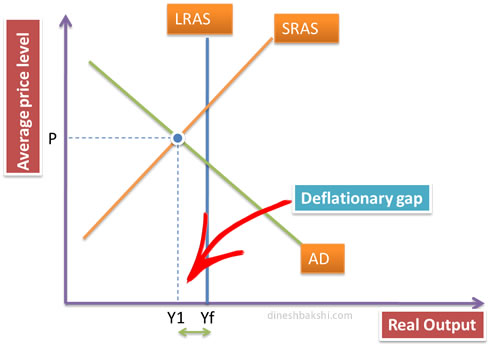

Fall in aggregate demand from AD1 to AD2 results in a fall in the level of national output from Yf to Y1

The economy experiences a deflationary gap

Deflationary gap: where the economy would be in equilibrium at a level of output that is less than the full employment level of output

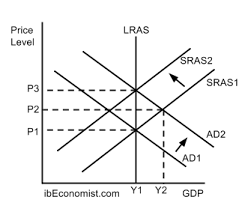

Long run equilibrium in classical model:

Fall in price level means that the prices of the factors of production have fallen

Unemployed workers will accept lower wages

Firm’s cost of production will fall which results in shift in the short run AS from SRAS1 to SRAS2

Lower factor costs = more production

As a result, the economy will return to its long run equilibrium at the full unemployment level of output, at a lower price level

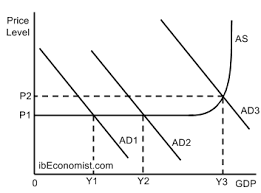

Regular long run equilibrium:

Output can increase along the short run AS curve by having workers work overtime (short-term solution)

Excess demand creates inflation (P1-P2), so wages increase to match this inflation

Increased cost of production

Firms reduce output and the economy returns to Y1

Limitations of the classical model:

LR equilibrium will always be at full employment (is at its maximum potential)

There is no need for demand management in terms of recession

Increasing demand can only cause inflation in the long run

The Keynesian Theory: Suggests that if wages do not change, there will be no difference between the short run and long run

If the economy ha large space capacity then any increase in output is likely without an increase in input prices and final prices

If the economy is near full employment, workers will want higher wages. Output and inflation increase

Supply side policies: government attempts to increase productivity and efficiency in the economy

Keynesian: during a recession, supply-side policies may increase productive potential however no actual growth occurs

Classical: supply-side policies are very important as they do not create actual and potential economic growth, but also decrease inflation